Q4 2017 – “Expect More of the Same in 2018″

Q4 2017 – “Expect More of the Same in 2018″

Investors throughout the world had much to cheer this past New Year’s celebration, as positive returns were experienced by investors throughout all markets. Stocks in the U.S. had their best year since 2013 as the S&P 500 Index returned 21.8% with December marking 14 consecutive months of positive returns, a feat not achieved since 1970. Strong performance was not confined to the U.S. as most of the major global equity markets posted double-digit returns as well.

Fixed income investors also enjoyed another positive year. While total returns for fixed income investments were not as high as those achieved in 2016, the market was significantly less volatile and the high yield market did not experience any significant sell-offs throughout 2017. It was another year where investors ventured out on the risk spectrum in pursuit of higher yields, and as a result lower credit quality “riskier” bonds outperformed higher credit quality “safer” bonds during the period.

One of the rare tailwinds that provided momentum for investors was that all of the world’s biggest economies experienced growth at the same time, a phenomenon described by economists as “synchronized global growth”, which continues today. In spite of the numerous geopolitical issues facing the world last year, nearly all regions had positive economic growth in a low inflationary environment, which we believe will provide a good backdrop for investors in 2018.

While healthcare reform in the U.S. remained elusive last year, Congress was successful in passing tax reform that should place U.S. companies in a better competitive position within the global economy. Over the past 30 years almost every developed country, with the exception of the U.S., had cut its corporate tax rate to attract investment. U.S.-based companies were increasingly disadvantaged by our domestic corporate tax policy and therefore many sought to reincorporate in low-tax countries in order to compete more effectively in the global marketplace. With the permanent reduction of the corporate tax rate from 35% to 21%, suddenly the world’s biggest economy has a tax policy similar to other developed economies. This is great news for the market. Additionally, a provision of the tax overhaul will allow U.S. companies to bring back cash that has been parked overseas to avoid higher taxes with a lower one-time cut for repatriation of earnings and cash. While U.S. companies have nearly $3 trillion in cash held overseas, it is estimated that nearly $400 billion could be brought back to the U.S. in 2018. While some countries are nervous about how a lower U.S. corporate tax rate could affect their respective attractiveness to investment capital, the entire world should benefit when the world’s largest economy is healthy. While tax reform aids Corporate America to the greatest extent, most individuals will benefit from lower taxes as well, but only temporarily as the reductions are scheduled to phase out after 2025.

In addition to the tax cuts, deregulation has been a significant priority of the Trump Administration, as the regulatory state is rolling back at a pace faster than even Ronald Reagan achieved during his Presidency. This follows years of expanding regulatory burden, with President Obama presiding over six of the seven highest annual page count increases to the Federal Register, where new regulatory rules are published. While it is difficult to fully understand the impact that the past decade of regulatory expansion has had on businesses, the Trump Administration projected that regulation took a $1.9 trillion annual toll on the economy in 2016. For Corporate America, there is a lot to look forward to in 2018.

The employment picture continues to strengthen with the economy posting a record 87 consecutive months of job growth and an unemployment rate of only 4.1%, a 17-year low. Consumer confidence is high which promotes an environment where consumers are willing to spend. Evidence of that was confirmed late December, when Mastercard reported that this past holiday season was the largest year-over-year increase since 2011 and set a new record for total dollars spent. Since consumer spending accounts for 2/3 of the U.S. economy, a healthy consumer and increasing sentiment should help economic expansion continue throughout 2018.

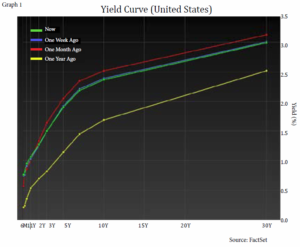

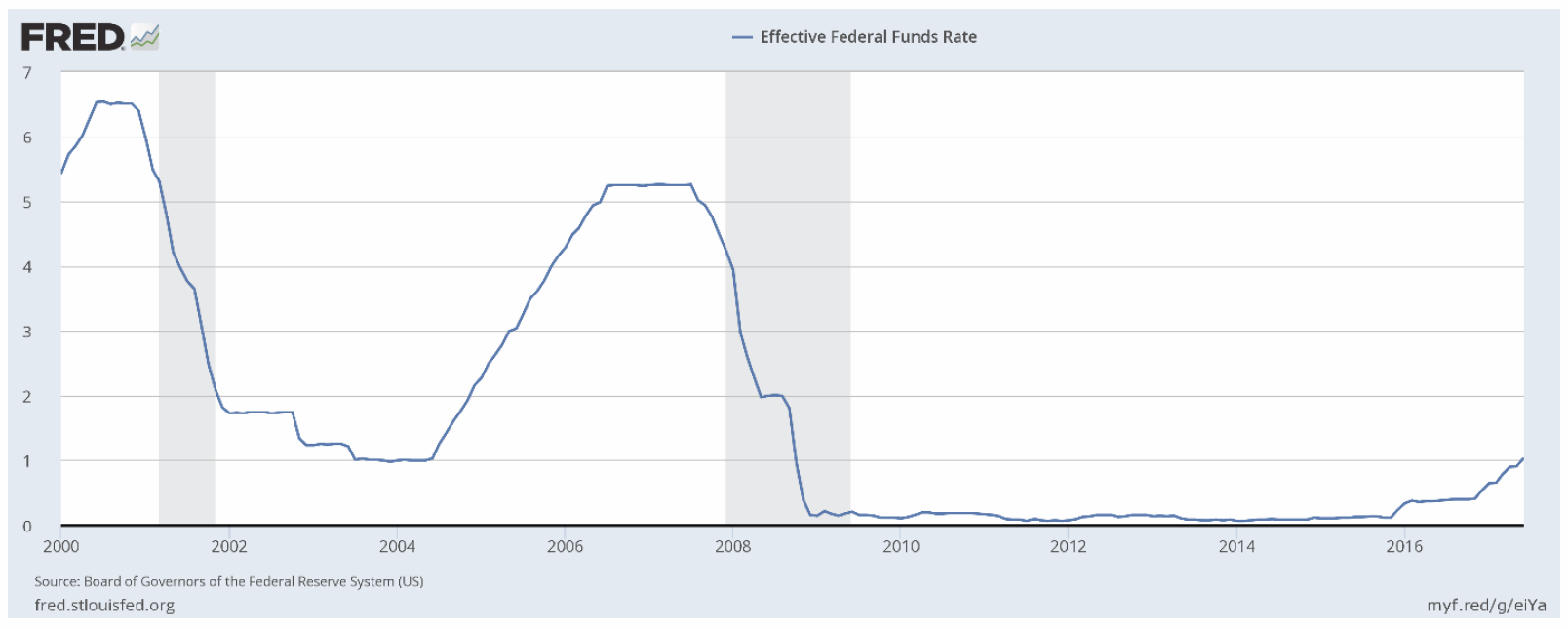

Long-term interest rates have remained subdued even with the Fed’s three short-term rate increases in 2017. The result has been a flattening of the yield curve over the past year where short-term rates have risen while long-term rates moved downward. For example, the 10-Year Treasury note, a common measure of long-term rates, yielded 2.56% at the end of 2016 but finished 2017 lower at 2.43%. Most forecasts anticipate three rate increases by the Fed this year, but if the economy starts to show signs of overheating the Fed may be forced to raise rates at a greater frequency, which could pressure stocks as investors sell riskier assets and gravitate towards higher yielding fixed income securities.

While yield spreads for non-investment grade bonds offer little room for error, in our opinion, the high yield asset class could deliver low to mid-single digit returns in 2018 due to continued strength in underlying business fundamentals and corporate tax reform, which should improve credit metrics and keep default rates low. We believe corporate high yield bonds offer a more favorable risk/reward profile relative to certain other traditional fixed income investments (e.g., Treasuries and other government bonds). Higher coupon rates and lower interest rate sensitivity characteristics (duration) of high yield corporate bonds provide some buffer to potentially mitigate the eroding effect higher interest rates have on traditional fixed income securities. The primary headwind for corporate credit is that current yields have already discounted some of this good news. We continue to favor high yield bonds on the higher-end of the credit quality spectrum and bonds with shorter maturities, both of which are less sensitive to interest rate movements.

As global economy enters 2018, it is likely that more of the world’s central banks will start to unwind the extreme stimulus measures that have been in place for nearly the past decade. This process is already under way in the U.S.; however the central banks in Europe have been reluctant to follow, thus far, despite the world’s synchronized economic expansion. Even as economists in Europe have increased that region’s economic growth expectations for 2018, the European Central Bank (ECB) plans to continue injecting $35.5 billion into the economy each month through its current quantitative easing program. ECB’s economists projected in December that the eurozone’s economy will grow 2.3% in 2018, a big increase from the 1.8% growth projected as recently as this past September.

A final thought that investors should consider with their investments as we look out into 2018 centers around the passive versus active management debate, or “indexing” trend that continues to garner media attention. Last year marked the conclusion of Warren Buffet’s bet that hedge funds would underperform an S&P 500 Index fund over a 10-year period. He won and hedge funds lost. While it makes great fodder for the media, this bet had multiple problems when used as evidence for comparing active management vs. passive investing. For starters, hedge funds are not traditional investment vehicles one should think of as active management. High minimum investment amounts, a lack of liquidity lock-up periods which tie up investor capital for years combined with complicated and often murky investment strategies make most hedge funds unsuitable for the typical Main Street investor. The result of this 10-year bet detracts from the debate of whether or not traditional actively management strategies (e.g., mutual funds or private client individual investment strategies) are value creators when compared to index funds and ETFs.

What you won’t see communicated in articles written about the brilliance of Warren’s bet is that Berkshire Hathaway (ticker BRK.A or BRK.B), the multi-national conglomerate holding company that he leads at the helm, also did not beat the Vanguard 500 Index Fund that he selected for the hedge fund bet. Surely he isn’t advocating that Berkshire shareholders sell their stock and invest in an index fund.

According to our analysis using the eVestment database, the most popular repository of fund and institutional investment strategies available to U.S. investors, approximately $2.4 trillion dollars is currently invested in passive index products that are designed to track the S&P 500 Index. That is a significant amount of wealth that is guaranteed to underperform the benchmark 100% of the time (net of fees). Recall that while passive investing is lower cost, it isn’t free which guarantees a return below the S&P 500. We believe a significant portion of the passive investing movement has been driven by certain financial advisors and “robo advisor” programs that are charging their own fee of 1% or more on assets. This management fee is in addition to the investment expense deducted by the underlying index fund. We note that in 2017, almost 50% of U.S. active equity mutual funds beat their benchmarks, after fees according to data compiled by Credit Suisse. Independent investment research firm, Morningstar, makes it relatively easy to compare mutual funds to the S&P 500 on their website (www.morningstar.com). The results may surprise you. Active management isn’t nearly a value-detractor as portrayed in the media. Finally, the majority of equity funds created by, and managed by, Kornitzer Capital Management have outperformed the S&P 500 Index over the past 10 years, net of fees.

From a market risk perspective, we remain concerned about the influence that passive investments, such as ETFs and index funds, could have on stock prices in a volatile market. Barron’s recently mentioned a point that the dramatic increase of passive investments have put a large amount of stock ownership that isn’t tied to the fundamental performance of the company, nor its valuation. For instance, Vanguard Group owns 5% or more of 491 companies in the S&P 500, up from 116 in 2010.

From a market risk perspective, we remain concerned about the influence that passive investments, such as ETFs and index funds, could have on stock prices in a volatile market. Barron’s recently mentioned a point that the dramatic increase of passive investments have put a large amount of stock ownership that isn’t tied to the fundamental performance of the company, nor its valuation. For instance, Vanguard Group owns 5% or more of 491 companies in the S&P 500, up from 116 in 2010.